By PATRICK FOGARTY //

The real estate industry is in flux – but there are significant opportunities across all sectors.

![]() Investment strategies must be revisited, reimagined and redeveloped to succeed in this rapidly changing marketplace. Implementation must be timely and costs must remain within budget.

Investment strategies must be revisited, reimagined and redeveloped to succeed in this rapidly changing marketplace. Implementation must be timely and costs must remain within budget.

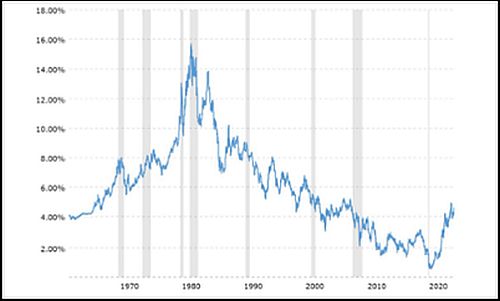

While a long-term look reveals that federal interest rates are still near historic lows, they have risen by nearly 5 percent since 2020, a significant change that has impacted property values. It’s essential to be prepared for the possibility that current rates will remain elevated and may not return to recent lows anytime soon – underscoring the need for strategic planning and adaptability in changing financial landscapes.

The destruction of value to certain investments has resulted in an investment pause and a significant “dry powder” supply of venture capital waiting to be deployed. Some estimates place the amount of available VC at more than $300 billion, reflecting a potential trillion-dollar value when combined with leverage.

Patrick Fogarty: Challenge accepted.

However, as higher-yielding strategies have been first to deploy – such as the shift to private credit – most equity remains on the sidelines, waiting for values to bottom out.

Equity is further stifled by dislocations in the banking sector (a general caution toward CRE lending), which begs the crucial question of “how much, when and where” capital will be deployed next.

Pressures in the housing sector evidence a need for more inventory. But can investor risk/reward returns be achieved? Historically, the market for single-family home development was separate from the rental-housing market. Today, however, we see institutional ownership invested heavily in both.

On Long Island, we have a housing shortage of more than 100,000 units. Great strides have been made in transforming downtown areas with transit-oriented developments, but the market is still woefully short on meeting overall demand – while extended approval processes and a lack of available land have pushed many developers to seek opportunities outside the region.

The post-COVID work-from-home environment has created significant vacancies in secondary and tertiary segments of the office market. In reimagining the future of office property, can developers make economic sense of adaptive-reuse strategies (office to residential)? Can they complete these projects promptly to meet demand? Will developers create more live/work space or amenitize existing office space to accommodate these trends?

Very interesting: Interest rates are still near all-time lows, but have been rising in recent years, creating a distinct real estate challenge. (Source: Real Estate Institute at Stony Brook University)

Industrial warehouse distribution performed well before and during COVID, proliferating product types from cold storage to logistics to last-mile fulfillment. However, it now appears we are at a saturation point. A shift to data centers and facilities supporting artificial-intelligence growth now dominates the landscape. But can we source all the necessary components from the supply chain to meet the development challenge?

The hospitality industry faces many challenges. Sustainability efforts, changing consumer preferences, safety and security, political instability, a shortage of talent and limited worker housing all persist.

In retail, you must consider brick-and-mortar locations, direct sales by mail and e-commerce – today you can get your groceries, books and just about everything else from malls, big box stores, discount chains, mom-and-pop retailers or e-commerce websites.

Centers of attention: Where warehouses once proliferated, AI-focused data centers now dominate.

Retailers must embrace these multiple platforms, in a changing industry that now depends heavily on customer service and a better “shopping experience.” Significant investment in technology and data management is essential to understanding customer behaviors and adopting business strategies to capture and maintain customer relationships.

Demand currently outpaces supply in the medical/life sciences sector, supported by low vacancies and increased rental rates. However, construction costs continue to climb and labor shortages exist – even the medical sector is not immune to disruptions in the capital markets.

Marketplace consolidations, inflation, increased demand for services and supply-chain challenges have left many institutions scrambling for funding. As the real estate industry transforms, we can observe how new industry leaders will establish and follow their investment strategies.

No matter the risk/reward strategy deployed, developers must have a deep understanding of their market, customers and budgets, and how to deliver a finished product. Teamwork is essential. The opportunities are there but factors are certainly in flux – these are exciting and interesting times!

Patrick Fogarty is chairman of the Real Estate Institute at Stony Brook University and President at Fogarty Advisory Services.