By JENNIFER CONA //

A new federal tax deduction for adults ages 65 and older is welcome relief – especially on Long Island, where the cost of living continues to climb – but in some cases, the impact may be limited.

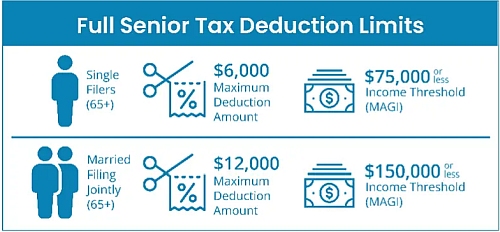

![]() Beginning with the 2025 tax year, eligible seniors can claim an additional $6,000 deduction, or $12,000 for married couples filing jointly, with full benefits available under certain income thresholds.

Beginning with the 2025 tax year, eligible seniors can claim an additional $6,000 deduction, or $12,000 for married couples filing jointly, with full benefits available under certain income thresholds.

On its face, that sounds like a straightforward win. But for many Long Island families, the reality is more nuanced.

Tax savings don’t exist in a vacuum. For older adults – especially those thinking about long-term care, Medicaid eligibility and estate-planning – every financial decision is interconnected. A deduction that lowers taxable income may help at filing time, but it doesn’t typically change the bigger financial picture.

In New York, where healthcare and long-term care costs remain among the highest in the nation, planning decisions often hinge on asset protection, not just annual tax strategy. In fact, the two are often antithetical.

Jennifer Cona: Big picture.

There’s also the question of who truly benefits. The deduction phases out at higher income levels, meaning many middle- and upper-income Long Island retirees may see only partial savings – or none at all.

Meanwhile, lower-income seniors – who arguably need the most support – may already have little tax liability to offset. The result is a policy that offers help, but not always where it’s needed most.

This moment also reflects a broader shift in how we think about financial planning. Families are no longer asking just what they can save this year; they’re asking how today’s decisions affect their future, their care and their ability to protect what they’ve worked for.

That requires a more integrated approach, where tax strategy is just one piece of a much larger plan.

At the same time, financial vulnerability among older adults is rising. Seniors are increasingly targeted for tax-related identity theft and scams, particularly during filing season.

On Long Island, where many older adults manage their finances independently, that risk is real – and growing. Any conversation about tax savings should also include steps to protect personal and financial information.

Moving parts: How much seniors can deduct depends on multiple variables. (Source: Focus Partners)

The takeaway isn’t that this tax break lacks value. It does offer meaningful savings for some. But its true impact depends on how it fits into a broader estate- and asset-protection plan.

For Long Island families, this is a reminder that smart planning isn’t just about reacting to new policies. It’s about understanding how those policies connect to long-term goals.

In today’s environment, that kind of forward-thinking approach isn’t just helpful. It’s essential.

Jennifer Cona is founder and managing partner at Cona Elder Law.